Consumer Service

- SYSTEM FOR FINANCIAL CONSUMER SERVICE

Petitions, Complaints, Claims and Suggestions:

To read the regulations on the financial consumer.

One of the mechanisms that Almacafé customers have to file complaints or claims regarding the quality of the services provided by Almacafé is to approach the Financial Consumer Ombudsman (Defensor del Consumidor Financiero), who will guide them and issue an objective, free, and independent ruling on the observations concerning the quality of Almacafé’s services that are brought before him.

Filing a complaint with the Financial Consumer Ombudsman does not require any formalities; it is sufficient to state the reason for the complaint, describing the facts and the rights considered violated, as well as the identification and other data that allow contact with the person filing the complaint to send them the corresponding response.

The Financial Consumer Ombudsman for Almacafé is provided by the company Serna Rojas Asociados and can be contacted through the following channels:

- Principal Ombudsman: Carlos Mario Serna Jaramillo

- Alternate Ombudsman: Patricia Amelia Rojas Amezquita

- Telephone: PBX 601 4898285 Monday to Friday from 8:00 a.m. to 5:30 p.m.

- Website: www.defensoriasernarojas.com

- Complaint Filing (7/24 Reception):

- Option 1: Main Screen / Send your complaint

- Option 2: Ombudsman Tab / Send your claim

- E-mail: defensoria@defensoriasernarojas.com

- Physical Address: Carrera 16 A No 80-63 office 601. Edificio Torre Oval.

- Hours of Operation: Monday to Friday from 8:00 am to 12:00 pm and from 2:00 pm to 5:00 pm.

The service offers that Almacafé supplies for the customers’ information are the conditions under which it will provide the different services, such as: general warehouse for goods and merchandise storage, customs brokerage and the delivery of the financial services offered by the institution.

Almacafé maintains a financial education strategy aimed at its Clients, regarding the different operations, services, markets, and types of activity it develops, promoting that they can make informed decisions and know the different mechanisms for the protection of their rights, as well as the various self-protection practices.

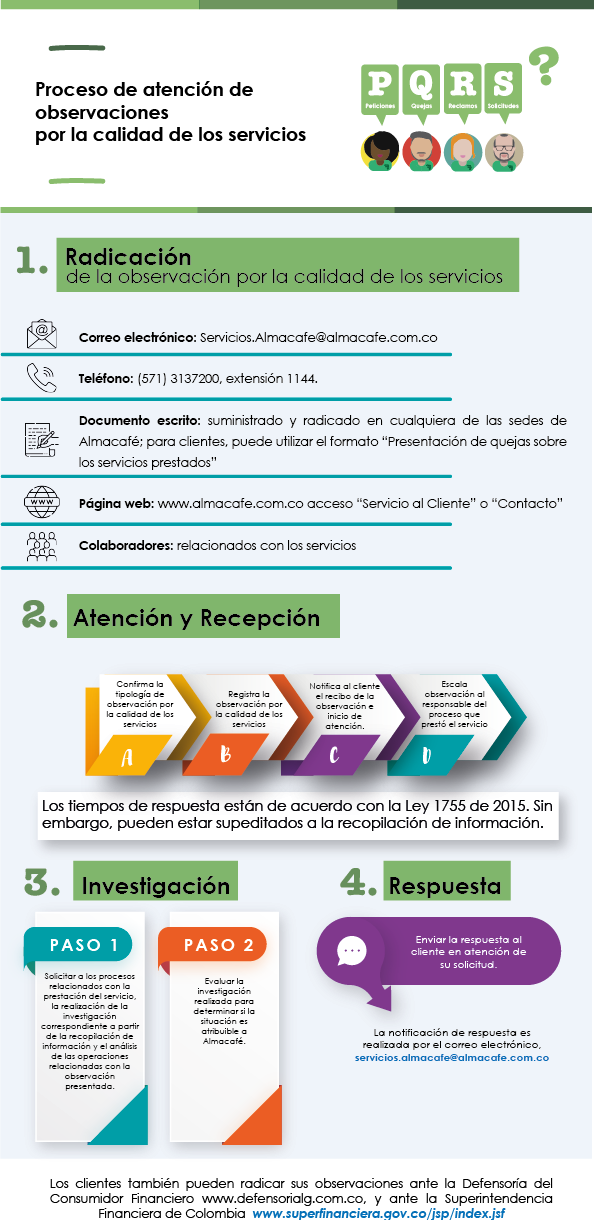

We work every day to improve our services. Please let us know about your experience with us through:

Email: servicios.almacafe@almacafe.com.co

Office hours: Mon – Fri: 8:00 a.m. – 12:00 p.m. and 2:00 p.m. to 5:00 p.m.

Phone: (571) 3137200, extension 1144

Office hours: Mon – Fri: 8:00 a.m. – 12:00 p.m. and 2:00 p.m. to 5:00 p.m.

- Form available at our offices for submitting complaints about services rendered.

- Website: “Customer Service” or “Contact” section.

- Employees related to the services.

- Through the Superintendencia Financiera de Colombia: https://www.superfinanciera.gov.co/jsp/index.jsf

The service contracts of Almacafé will be adjusted according to the service conditions requested by the client, considering that our offers are adapted to customer knowledge and the specific needs of both their relevant sector and specific activity.